Hello!

Nearly 107,000 bitcoin have been moved since early Asian hours on Tuesday, with bitcoin shedding 1.2% on expectations of selling pressure.

Wallets belonging to the defunct Bitcoin exchange Mt. Gox transferred over 140,000 bitcoin (BTC), valued at around $9 billion, to an unknown address starting early Asian morning hours on Tuesday.

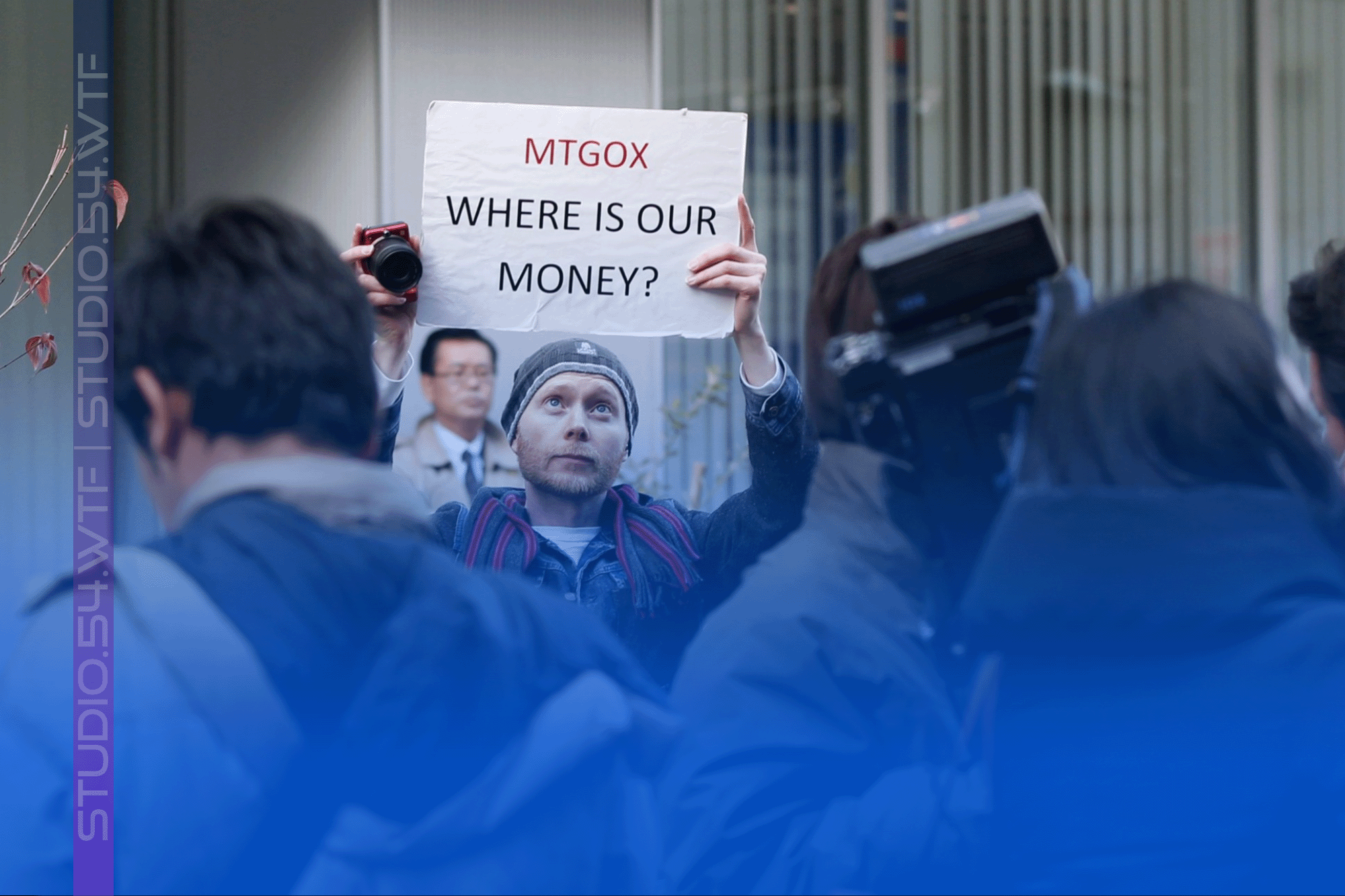

Mt. Gox, once the largest bitcoin exchange in the world, closed in 2014 after it was revealed that it had lost hundreds of thousands of bitcoin in a hack. Creditors have since awaited the repayment of their holdings - one that is largely considered to add selling pressure to BTC markets.

In a press release, rehabilitation trustee Nobuaki Kobayashi said that no sale of bitcoin or bitcoin cash (BCH) had taken place and that the group was "managing bitcoin and bitcoin cash in a secure manner."

Wallet activity shows the movements were done over thirteen transactions. A likely test transaction worth $3 was made on May 20, and another smaller transaction of $160 was done early Tuesday. The remaining transactions ranged from $1.2 million to $2.2 billion worth of bitcoin.

All of Mt.Gox's bitcoin has now effectively been moved to a single bitcoin wallet, Bitinfocharts data shows.

This is the first movement of assets from Mt. Gox's cold wallets in over five years and is likely a part of a plan to distribute the assets back to creditors before October 31, 2024.

All coins have been transferred to a new address “1JbezDVd9VsK9o1Ga9UqLydeuEvhKLAPs6,” CryptoQuant head of research Julio Moreno said in an X post.

Alex Thorn, head of research at Galaxy, said in an X post that he expected most of the transferred bitcoin to be held by creditors, instead of being sold on the open market.

Still, market participants appeared to turn bearish on the movements with bitcoin shedding 1.4% since the start of Asian trading hours. It dropped to as low as $67,680 after a Monday high of over $70,000.

Source: Shaurya Malwa – coindesk.com