Hello!

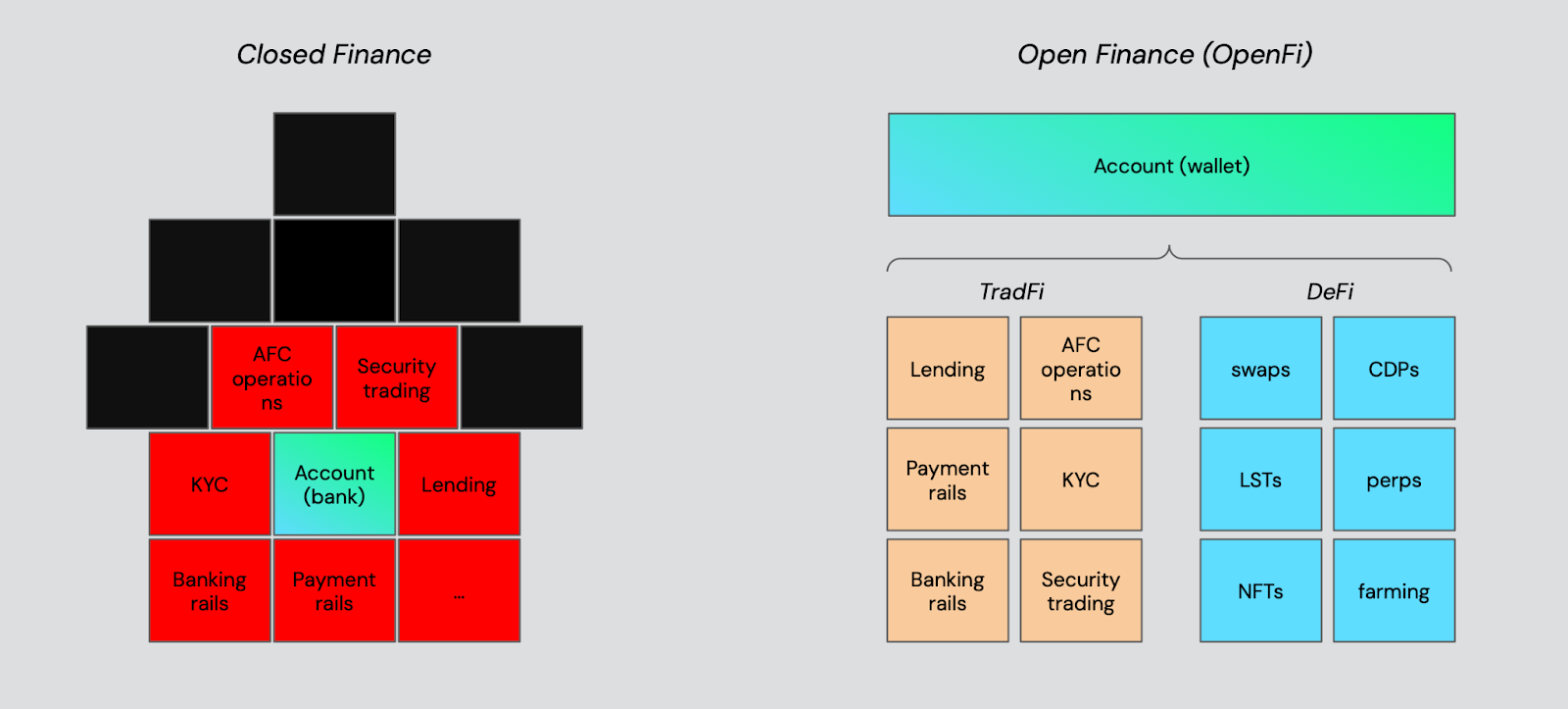

“OpenFi” aims to unbundle to take the “account” out of bank account

In the early 2010s, banking customers dissatisfied with the fees, complexity and poor service of traditional banks gained some new options.

Neobanks, also called digital or challenger banks, emerged as fintech startups aimed at providing banking services primarily through mobile apps and web platforms, without the need for physical branches.

Fintechs like Simple in the US, N26 in Germany, and Monzo and Revolut in the UK focused on providing an intuitive user experience, often incorporating features such as real-time spending notifications, budgeting tools and easy money transfers.

Yet like their brick and mortar counterparts, there remains an account at the center of a closed loop of services.

A new crypto consortium is pitching “Open Finance,” or OpenFi, as an alternative to both neobanks and strictly crypto DeFi.

The key concept lies in starting from a user-controlled account. Rather than having banks as the KYC-enforcing gatekeeper, banking services can be plugged in — and swapped out — like the “money Lego” metaphor we’re so accustomed to in Web3.

In short, OpenFi is a framework for integrating noncustodial blockchain solutions into the traditional financial system.

Pitched on the sidelines of EthCC in Brussels, the group envisions a future where banking accounts are replaced by smart wallets, enabling users to manage their finances independent of any one centralized entity.

Instead, like an a la carte menu, specialized providers take on the job of banking services, an approach that removes single points of failure and puts users in control.

A key component of the OpenFi strategy is the development of infrastructure to support apps. As Jasper De Maere, research lead at Outlier Ventures noted, “apps inspire infrastructure [and] infrastructure enables new apps.” In short, it’s time fintechs migrate to a new tech stack, he said.

Unlike embedded wallets offered by centralized players — sometimes referred to as CeDeFi, OpenFi advocates call for the use of smart wallets — Safe and Zeal, which is built on Safe, are two of the group’s initial members.

Smart accounts provide direct access to DeFi applications, allowing users to determine their security setup, while outsourcing payment and banking rails to providers such as Monerium and Gnosis Pay.

For OpenFi to realize its full potential, there needs to be a concerted effort to develop more user-friendly applications that can rival those offered by traditional fintech companies, but also further progress on identity and security solutions.

On the identity front, Julian Leitloff of idOS pointed to the need to streamline onboarding and avoid redundant KYC processes. Today, most users need to repeatedly verify their identity when accessing different financial services. OpenFi, which Leitloff called “the killer use case for crypto,” proposes a unified identity solution that simplifies this process.

The idOS system uses an Arbitrum Orbit chain but is chain-agnostic, and provides user-encrypted data to dapps via an SDK.

Despite the promise of OpenFi, traditional financial institutions will continue to play a crucial role, according to Julian Grigo from Safe. Merchants and service providers are not yet ready to accept direct crypto payments, which is why hybrid solutions like Stripe, Gnosis Pay and Kulipa are needed to bridge this gap while maintaining regulatory compliance.

But by unbundling accounts from banking services, the OpenFi group hopes to fulfill the promise of an open, user-centric financial ecosystem, with greater choice and more options for generating yield onchain — something the neobanks have failed to deliver.

Source: Macauley Peterson – blockworks.co